Roger Debreceny

Shidler College Distinguished Professor of Accounting

Shidler College of Business

University of Hawai'i at Manoa

Google Voice: +1 (513) 393-9393

roger@debreceny.com rogersd@hawaii.edu

www.debreceny.com

www.twitter.com/debreceny

I have been involved with research and development on XBRL since my co-authored conference paper presented at the 1998 Annual Meeting of the American Accounting Association, subsequently published in the International Journal of Accounting Information Systems. More recently I co-chaired with Prof. Bill McCarthy of Michigan State University the Workshop on Ontological Specification of Interoperability Semantics for Financial Information and Business Reporting Systems funded by the National Science Foundation. The workshop was held in May 2008 covered somewhat similar ground to that of the W3C/XBRL workshop (http://nsfaccountingontology.wik.is/Workshop). I am focused on issues such as taxonomy quality and interoperability and the impact of XBRL and similar technologies on the disclosure environment for private and public entities internationally.

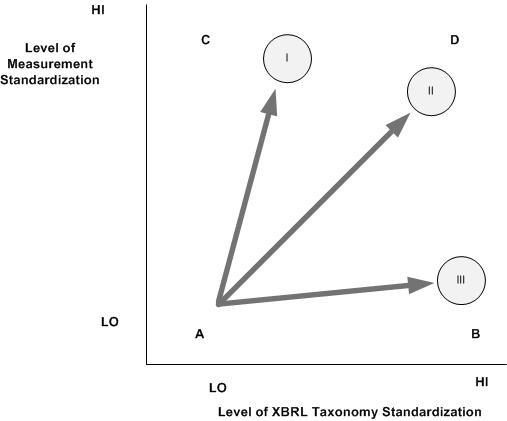

I illustrate some of these design challenges in the following Figure.

Four conditions are possible. At Condition A, there is low content and taxonomy standardization. The probability that information coming from different taxonomies in this combination can be compared is low. Moving along vector III to Condition B brings a very high standardization level of XBRL taxonomies. While there may be different underlying measurement techniques, there will be high levels of comparability of concepts. For example, construction of identical taxonomies for US GAAP and IFRS will allow comparison at the concept level. It will not allow reconciliation of different measurement techniques. Condition C has a high degree of measurement comparability but low levels of standardization at the taxonomy level. For example, the concept of is defined within the International System of Units. Yet, we could have taxonomies that each represented kilojoules in mutually incomprehensible fashions. The highest Level is condition D. Here we see high standardization of both taxonomy and content dimensions.

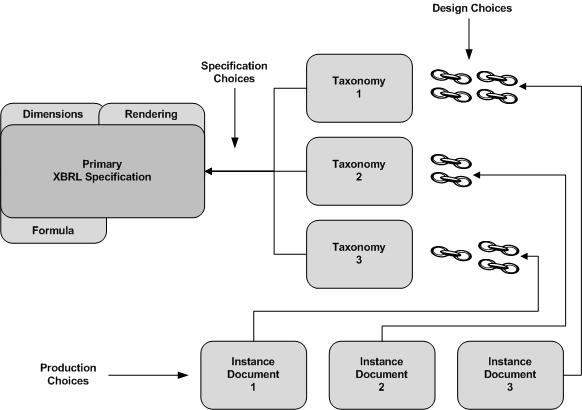

When considering standardization and XBRL adoption, it is important to consider the extension of existing taxonomies. When allowed, information providers can add additional elements to the core taxonomy and create a special extension. These additional elements are special to the information provider. Extensions can either help or hinder taxonomy standardization.

What comes from this analysis? First, when XBRL-based business-reporting solutions are proposed, there must be a clear understanding of the costs and benefits of flexibility. Flexibility in taxonomy design within the same knowledge domain is not, per se, undesirable. Rather, there are constraints on the extent of flexibility. Professional guidance, economic analysis and academic research are all necessary to understand the boundaries, costs and benefits of flexibility. Second, there is a clear need for research on the tools that can assist in appropriate taxonomy design that will maximize interconnectivity.

Some of the questions for information value chain integration include:

I view these issues from a perspective of an academic that works at the intersection of accounting, auditing, information systems and computer science. Each of these disciplines have very different research traditions, publication outcomes and performance metrics. Even within the small sub-discpline of accounting information systems, we see clear differences between those researchers that take a design science perspective and those that take a natural science perspective. Yet, there are so many unanswered questions, it will be important to engender research collaboration, communication and interaction research communities. Further, the intersection of these research communities with the W3C and XBRL practice communities is also important. I trust that these issues will be discussed at the workshop.

* Based in large part on Piechocki, M., C. Felden, A. Gräning, and R. Debreceny. 2009. Design and Standardization of XBRL Solutions for Governance and Transparency. International Journal of Disclosure and Governance 6 (3):224-240.

Roger Debreceny. roger@debreceny.com. 20 August 2009.